The GBTC Death Spiral: Is the Contagion Over?

The GBTC Death Spiral: Is the Contagion Over?

The hidden force behind the bear market and why it might signal that the bottom is in

You’ve heard about the collapses of FTX, Luna, Three Arrows Capital (3AC), BlockFi and other lenders. And you’ve heard about the weakness in the macro economy and how the Fed is raising interest rates to fight inflation which has hurt crypto.

These forces have certainly contributed to crypto’s bear market. However, there’s another major factor that has perhaps played an even bigger role in the bull and bear markets. It’s leverage on the Grayscale Bitcoin Trust (GBTC) arbitrage trade.

In this report, I cover how so much leverage got pumped into the GBTC arbitrage trade, the contagion it caused, and how GBTC is influencing the price of Bitcoin now.

Here’s the TLDR:

Excess leverage on the GBTC arbitrage trade added fuel to the bull market.

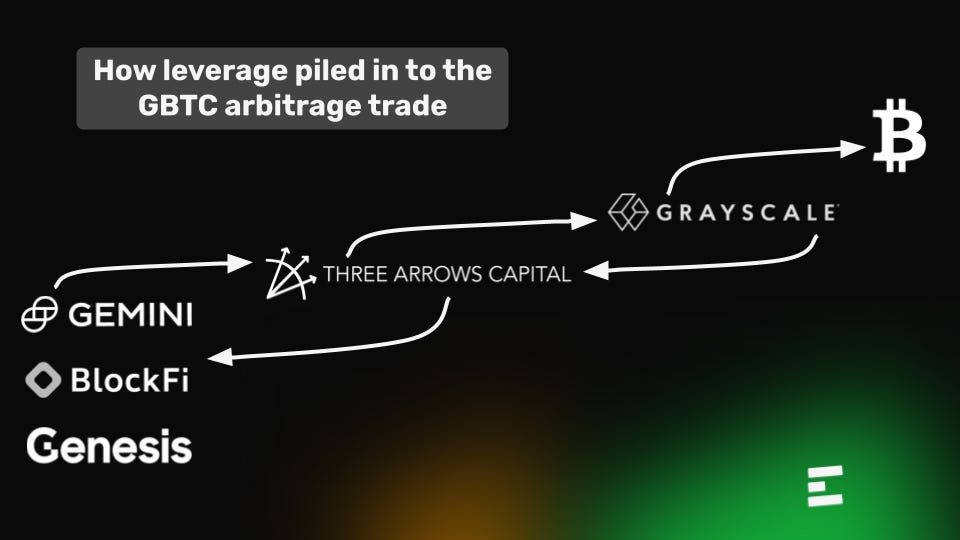

Crypto investors deposited their holdings onto lending platforms (BlockFi, Gemeni Earn, etc.), who lent to funds such as 3AC, who bought into Grayscale’s trust with leverage, who then bought up Bitcoin, sending the price of Bitcoin higher than it would have otherwise.

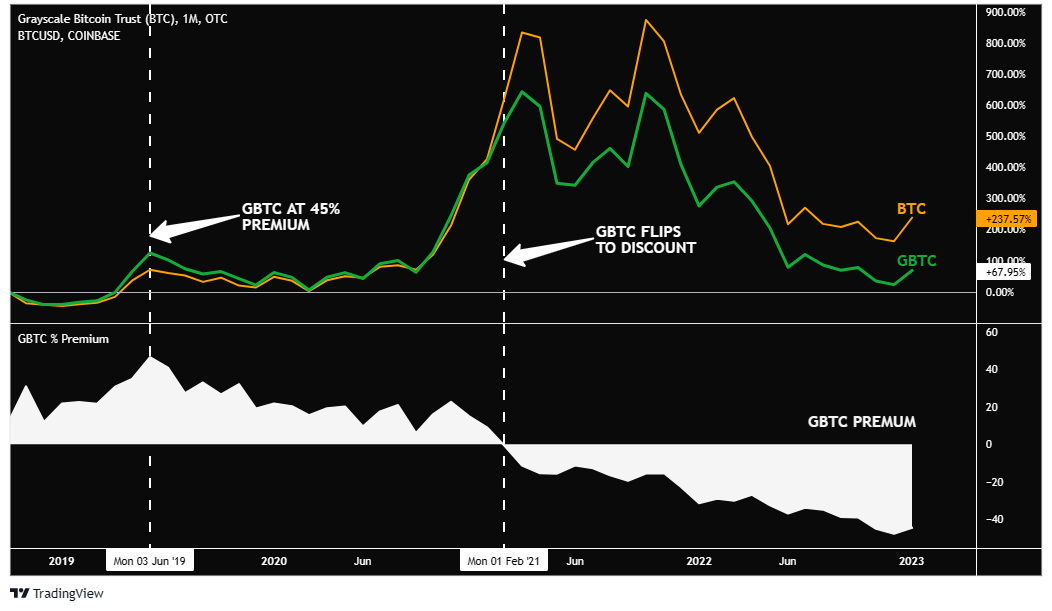

Forced selling of GBTC because of margin calls on excess leverage sent the trust from trading at a premium to the net asset value of its underlying Bitcoin to selling at a 50% discount. This likely extended the bear market.

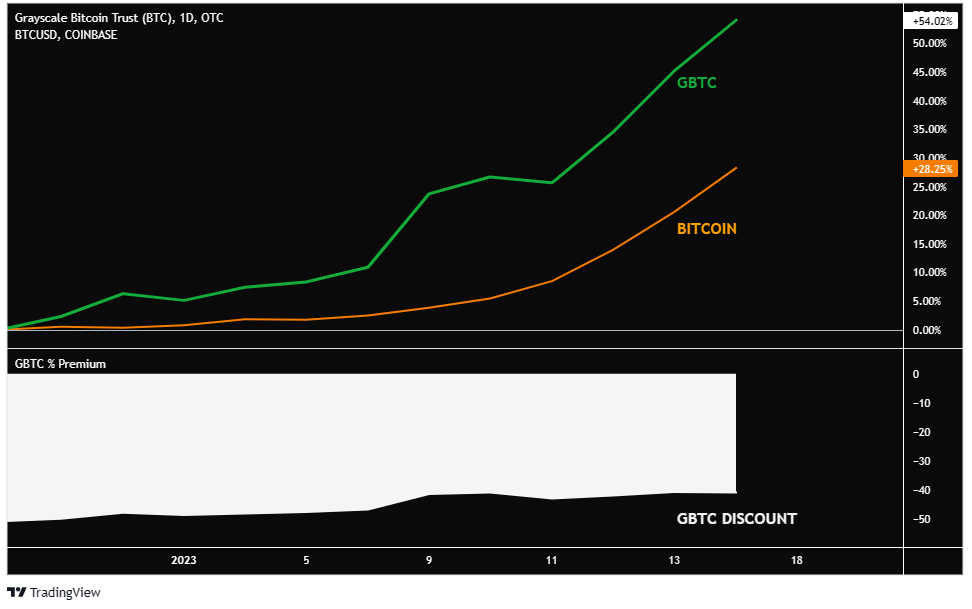

The GBTC discount is now narrowing, potentially indicating that the forced selling and the worst of the contagion may be almost over.

The GBTC Arbitrage Trade

GBTC is a trust managed by Grayscale, the largest digital currency asset manager. Grayscale is owned by Digital Currency Group (DCG), a crypto conglomerate and investment firm.

GBTC is primarily marketed towards institutional investors who couldn’t get direct exposure to Bitcoin because they can’t custody it themselves.

Institutional investors buy into the trust, Grayscale creates new shares, and buys and custodies Bitcoin to back the shares. GBTC shares trade publicly. Separately, retail investors can also buy shares in their retirement or brokerage accounts.

GBTC had been trading at a premium to its underlying Bitcoin for years. This allowed institutional investors to make a profit by arbitraging the price difference. The graph below shows the gap between GBTC and its net asset value during the 2017 bull market.

Institutional investors bought into the trust at a price that was at par to the underlying Bitcoin. After the six-month lock up period, they sold their shares on the open market at the premium price and profited the difference. The premium between the price of GBTC and the price of Bitcoin had historically been more than 20%.

The Hidden Force Behind the Bull Market

The bull market started in parallel with unprecedented quantitative easing (QE) to help contain the damage of Covid lockdowns. This included:

Reducing interest rates to 0% in March 2020

Increasing the US money supply (M2) by $6.4 trillion from February 2020 to January 2022

Increasing the US Central Bank balance sheet by $4.8 trillion (more than double) from February 2020 to January 2022

Increasing federal debt held by Federal Reserve banks by 150%

In addition to the QE, everyone was forced to stay home with nothing else to do besides get orange pilled and gamble their stimulus checks on stonks and crypto.

This was the perfect storm to kickstart the bull market. However, the crypto market was further accelerated by the leveraged buying that few knew was happening (until it fell apart).

Adding Leverage to the GBTC Arbitrage Trade

The GBTC arbitrage trade was easy money for years. So 3AC added leverage. They borrowed from lenders such as BlockFi to buy into the trust with even more capital.

Lending platforms like BlockFi’s deposits under management skyrocketed during the bull market. They offered crypto investors high interest rates on the crypto holdings they deposited. The rates were often over 10% APY, which was way more than you could get at a traditional bank because interest rates were so low. Inflation also began to pick up, so people needed to put their money to work to keep up with rising costs.

Some lenders also bought into GBTC directly to generate the yield that they promised to their depositors.

According to Messari CEO Ryan Selkis’ 2023 Theses, “3AC and BlockFi accumulated 10% of the Trust’s shares with $4 billion in exposure at the peak in February 2021.”

Gemeni Earn, another lending platform, lent about $900 million of their customers’ deposits to Genesis, a subsidiary of DCG. Genesis then lent $2.6 billion to 3AC.

The loans that lenders made to 3AC were undercollateralized. According to Sam Andrew, Author of Crypto Clarity, “The 3AC bankruptcy filing suggests that $1 billion of the Genesis loan was unsecured. Unsecured loans do not have collateral backing them”.

3AC then bought into GBTC with the loans given to them. The firm also used the GBTC shares that they bought as collateral to borrow more money and pile it into GBTC. 3AC owned 39 million shares of GBTC, worth $1.3 billion by the end of 2020.

At its peak in early 2021, Grayscale had $40 billion in assets under management. GBTC shares outstanding grew by over 200% during the bull market.

Grayscale Bought Bitcoin, Sending it Even Higher

As institutional investors like 3AC bought more GBTC with leverage, Grayscale bought more Bitcoin to keep the trust fully backed. In the chart below, you can see Grayscale’s Bitcoin holdings in blue.

According to Dylan LeClair, Head of Market Research at Bitcoin Magazine, “GBTC was the quiet biggest catalyst in the bull market." Grayscale bought 400,000 Bitcoin from the beginning of 2020 until the market topped in early 2021. Today, Grayscale still owns 3% of the total supply of Bitcoin.

There was additional leverage fueling the bull run. In an indirect way, FTX customer deposits were essentially used as leverage as they were given to Alameda to buy crypto. There was also leverage taken out by retail investors on exchanges.

The bull market pumped harder than it should have because retail investors deposited their crypto onto lending platforms like BlockFi, who then lent to 3AC, who then bought into Grayscale's Bitcoin Trust, who then bought massive amounts of Bitcoin.

Steven McClurg, Co-founder of Valkyrie, said in an interview on What Bitcoin Did: “A ton of leverage was created to pump the price. $69,000 wasn’t the right price for Bitcoin. That was a pumped, over-levered price.”

How the GBTC Death Spiral Started

The music eventually stopped. The GBTC premium flipped to a discount. Demand for GBTC shares decreased because investors had new ways to get exposure to Bitcoin and the market was getting toppy.

The GBTC shares that 3AC bought were trading at less than their net asset value. 3AC was in a losing trade.

In addition to the flip from premium to discount, a number of other negative events sent the crypto markets lower:

The QE that helped kickstart the bull market stopped, and the Fed started tightening. Interest rates increased, and the money supply, federal bank debt, and central bank balance sheet all decreased.

Luna and UST, its collateralized stablecoin, collapsed.

The SEC struck down DCG’s request to convert the GBTC trust to an ETF, which might have helped it maintain parity to its underlying assets.

FTX collapsed.

The Great Unwind

The GBTC that 3AC had posted as collateral decreased in value because Bitcoin started going down. The GBTC went down even more than Bitcoin because the premium flipped to discount. It was eventually trading at a nearly 50% discount to Bitcoin.

Lenders made margin calls on 3AC. Genesis took possession of 35 million GBTC shares. There was also a run on lending platforms such as BlockFi because of all the fear in the market. Customers withdrew funds in mass.

The GBTC investors who were attempting to arbitrage the premium were forced to sell.

Genesis took a substantial hit from the $2.3 billion loan it extended to 3AC. DCG bailed out its subsidiary, Genesis.

When GBTC started trading at a discount in early 2021, DCG started buying it to reduce the discount. DCG even borrowed $575 million from Genesis and used it to buy GBTC shares. DCG bought about 45 million shares between Q1 2021 and Q3 2022, according to the chart by Messari below.

“DCG was making a hedge fund-like trade, buying their own product on leverage,” said Ram Ahluwalia, CEO of crypto investment advisor Lumida Wealth in an interview with Forbes.

Grayscale had been a massive whale buyer of Bitcoin during the bull market. They stopped buying. That removed a major backstop on the price of Bitcoin.

DCG also started shorting Bitcoin to hedge their GBTC position. According to DCG’s Shareholder Letter published on January 10th, “DCG’s investment entity used the BTC borrowed from Genesis Capital to hedge GBTC long positions to remain market neutral on such positions.”

Valkyrie and BlockTower Come to the Rescue

Investors were spooked by GBTC trading at a 50% discount to the underlying assets that it holds. Some worry that the discount indicates that Grayscale may not be holding all of the Bitcoin (similar to the FTX debacle), or that Grayscale’s parent company, DCG, may be in such bad financial shape that they will need to shut down GBTC and sell the Bitcoin into the market.

Other investors see opportunity. Valkyrie, a digital asset manager, has launched a new fund that “seeks, among other things, to take advantage of the massive discount in the spread between the NAV and price of GBTC.” Valkyrie is also proposing that they take over management of GBTC, lower the management fees from 200 basis points to 75 basis points, and attempt to offer redemptions to investors in both Bitcoin and cash.

BlockTower, an institutional investment firm, has bought more than $10 million of GBTC recently.

3AC bought GBTC while it was at a premium as an arbitrage trade. Valkyrie and BlockTower are buying at a discount, betting that the discount will decrease because of the possibility for the trust to convert to an ETF, GBTC shareholders being able to redeem the underlying Bitcoin, or simply other market participants buying up shares.

It’s working for them so far. Per the chart above, GBTC has been outperforming Bitcoin this year as the discount has decreased from 50% to 40%.

How GBTC Impacts the Markets Going Forward

Fear over DCG’s financial situation and therefore over GBTC has been weighing the markets down. If DCG were to fail, it would have a ripple effect throughout the industry because they’re such a big player with so many different business lines.

There are still some potential worst-case scenarios looming (that I don’t think are particularly likely). If DCG or Genesis is forced to sell its GBTC or other crypto holdings to make their creditors whole, or is forced to liquidate GBTC, it would bring a lot of sell pressure into the market.

However, as the price of GBTC goes back up, DCG’s financial situation improves, and if DCG’s situation improves, the whole market improves. I believe that the narrowing of GBTC’s discount to its net asset value is a sign that the contagion throughout the industry might finally be close to resolved. There may not be as much sell pressure because everyone who was forced to sell or wanted to sell has already sold.

If the industry learns from this experience—about the risks of undercollateralized lending with volatile assets and excess leverage—I believe that the markets will be stronger going forward.